Grain Market Update - Wheat (May 2025)

Article provided by: Michael Jones, Grain Focus, Young

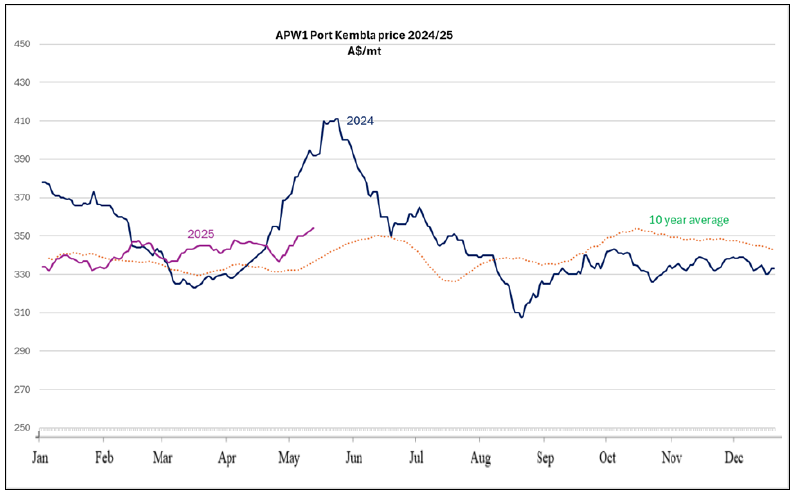

The Australian wheat market has not done a lot since harvest. The lower grades of wheat have performed the best, with prices lifting $35-$40/mt since harvest for ASW1 & SFW1. The bids for the milling grades have been flatter since harvest, with APW1 & H2 not showing as much change. The usual rule of thumb when deciding which grades of wheat to sell first, is to hold onto lowest quality grades and sell higher grades at harvest. This year has reaffirmed this rule.

Overseas wheat markets saw a brief rally in February on the back of production concerns in Russia and the US. There were fears that both crops could have suffered from the extremely cold conditions forecast at the time. It seems this fear was premature and since then, wheat markets have slipped back into the range they have been trading at since November. The international wheat markets have provided no reason for our market to rally so far this year. Importer demand for wheat has been routine, plus the ongoing US tariff situation is also keeping buyers reluctant to make big purchases, in case the overall situation suddenly changes.

Looking forward to the next crop - 2025/26 season APW1 Multigrade wheat was bid at $365/mt Port Kembla at the time of writing. Looking back at the past 5-year price range, this is at a Decile 4 which is not very enticing for making forward sales this early in the season.

Upside potential

It is now that time of the year where the grain market’s focus turns to the weather. Northern hemisphere spring grown crops are now in the ground and the next few months will be very important for crop development. US stocks of corn are currently at a three-year low and a big crop is needed to replenish supply. The coming few months are when the grain markets often see their highest volatility, as weather determines crop potential or demise.

The drop in the A$ of US4c earlier in April, gave the Australian market a boost as it makes our exports cheaper to international buyers. Any future downside in the A$ will continue to support this market.

Graziers have been putting upward pressure on the barley market. Each dry week that goes by means more livestock feeding. This has also rubbed off onto the wheat market. Domestic end users seem to have their requirements covered for the next few months. If it is still dry when they need to buy more wheat, even more upwards pressure on wheat prices could be seen.

Global wheat stocks are forecast to fall for the fourth time in five years. This leaves the market primed for a rally, if there is a production scare in one of the major exporting countries.

The major wheat growing regions of China are currently dry, which is being closely watched by the market. Any shortfall in China’s production, could see them importing large volumes of wheat.

Downside potential

The NSW 2024/25 winter crop harvest, proved to be solid. According to ABARES, even though total winter crop production was back 6% on the previous year, it was still 29% above the 10-year average and the second biggest on record. The north of the state and Queensland both had bumper harvests. Southern Queensland/northern NSW is where the majority of east coast feed grain consumption occurs.

Even though global wheat stocks are tight, there are factors offsetting this. US wheat stocks are plentiful, and crop conditions are currently good with harvest now only a few months away. Crop conditions are also mostly good in the EU and Black Sea region too. Until there is a weather scare that threatens 2025 wheat production in a major producing region, wheat prices are likely to trend sideways.

There has been a solid sorghum harvest in northern NSW/Queensland. Though sorghum is often not the preferred feed grain for feedlotters, this supply of sorghum could act as an anchor on the cereal grain market.

The information contained in this article is given for the purpose of providing general information only.